As the year comes to a close, many small business owners discover the same uncomfortable truth: their books aren’t as clean as they thought.

Uncategorized transactions, unreconciled bank accounts, unclear loan balances, payroll questions, and missing documentation tend to surface right when tax deadlines approach. Unfortunately, this is also when mistakes become the most expensive.

Year-end bookkeeping is not just about “closing the books.” It’s about accuracy, compliance, and giving your CPA reliable information so you don’t overpay taxes, understate income, or invite unnecessary scrutiny.

What “Year-End Bookkeeping” Really Means

Proper year-end bookkeeping goes far beyond running a profit and loss report. A true year-end review includes:

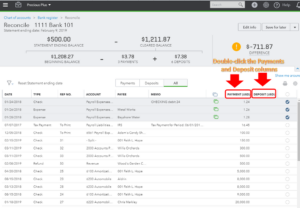

- Reconciling all bank and credit card accounts

- Verifying loan balances and amortization schedules

- Confirming payroll totals match W-2s, W-3s, and payroll reports

- Reviewing owner draws, distributions, and equity

- Ensuring expenses are properly categorized (not just “uncategorized” or guessed)

- Reviewing balance sheet accuracy, not just income

- Identifying missing documents before your CPA asks for them

If these steps are skipped or rushed, the risk shifts from inconvenience to real financial consequences.

Why Clean Books Save You Money

Messy books don’t just create stress — they cost money.

When transactions are misclassified or left unresolved:

- Deductions can be missed

- Income can be overstated

- Taxes can be calculated incorrectly

- CPAs spend extra time fixing issues (which you pay for)

- Financial decisions are made on unreliable data

Clean, reconciled books allow your CPA to focus on tax strategy, not cleanup. That’s where real savings happen.

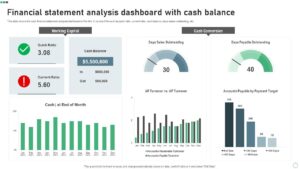

The Balance Sheet Is Not Optional

Many business owners focus only on the profit and loss statement. But the balance sheet is where problems hide.

Common year-end balance sheet issues include:

- Old loan balances that don’t match lender statements

- Credit cards showing incorrect or negative balances

- Payroll liabilities that were never cleared

- Owner contributions and draws recorded incorrectly

- Assets that were never properly capitalized

If the balance sheet is wrong, the entire set of books is unreliable — even if the profit looks reasonable.

CPA-Ready Books Matter

Your CPA depends on the accuracy of your bookkeeping. When books are incomplete or unclear, the CPA must make assumptions — and assumptions rarely benefit the taxpayer.

CPA-ready books mean:

- Clear documentation

- Reconciled accounts

- Properly classified transactions

- Confidence that the numbers reflect reality

This leads to faster tax preparation, fewer follow-up questions, and better outcomes.

Why Work With a Local Cleveland Bookkeeper

Working with a local bookkeeping firm means more than proximity. It means understanding:

- Local businesses and industries

- Ohio tax considerations

- Regional payroll and compliance issues

- The practical realities of small business operations

At Cleveland Bookkeeping, we don’t just “enter transactions.” We review, question, reconcile, and verify — because accuracy matters.

Get Ahead of Tax Season

The worst time to fix bookkeeping problems is when tax deadlines are looming. The best time is now.

If you’re unsure whether your books are truly ready — or you already know they aren’t — a year-end review can save time, money, and stress.

Schedule a consultation today and let’s make sure your books are accurate, complete, and CPA-ready before tax season begins.