Why Do We Reconcile to a Bank Statement? (And What Happens If You Don’t)

If you’ve ever wondered:

“Why do we even reconcile the bank account if the balance already looks right in QuickBooks?”

You’re not alone.

Many small business owners think reconciliation is just a bookkeeping formality. It’s not. It’s one of the most important financial control processes in your business.

Bank reconciliation is how you confirm that your financial records match reality.

And without it, your numbers can look accurate — while being completely wrong.

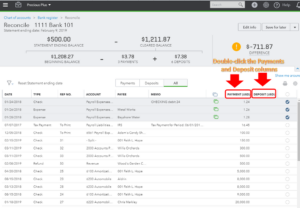

What Is Bank Reconciliation?

Bank reconciliation is the process of comparing:

Your QuickBooks register

Your bank statement

Cleared transactions

Deposits and withdrawals

To ensure they match exactly.

It confirms:

No transactions are missing

No duplicates exist

No amounts were altered

No fraud occurred

No bank errors happened

It is the foundation of financial accuracy.

Why Reconciliation Matters More Than Most Business Owners Realize

1️⃣ It Protects Against Errors

Bank feeds are not perfect.

Transactions can:

Duplicate

Auto-categorize incorrectly

Post to the wrong account

Be partially matched

Without reconciliation, these errors compound month after month.

2️⃣ It Prevents Financial Statement Distortion

If your bank account is off, then:

Your Profit & Loss is off

Your Balance Sheet is off

Your cash flow reporting is unreliable

That affects:

Loan approvals

Investor confidence

Tax preparation

Business decisions

Reconciliation stabilizes your financial foundation.

3️⃣ It Detects Fraud or Unauthorized Activity

Reconciling monthly helps identify:

Unauthorized charges

Unrecorded withdrawals

Payroll discrepancies

Missing deposits

The longer you wait, the harder it becomes to correct.

4️⃣ It Prevents Opening Balance Discrepancies

If you read our article on:

Opening Balance Doesn’t Match in QuickBooks

You already know that prior-period changes cause reconciliation issues.

Monthly reconciliation — combined with locked books — prevents this.

What Happens If You Don’t Reconcile?

Here’s what we see during clean-up projects:

Bank balances off by thousands

Duplicate deposits inflating revenue

Uncleared checks sitting for years

Misclassified loan payments

Prior reconciliations altered without documentation

At that point, it’s not maintenance.

It’s repair.

And repair is always more expensive than prevention.

How Often Should You Reconcile?

Minimum: Monthly.

Best practice:

Reconcile within 5–10 days of receiving the bank statement

Review reconciliation reports

Lock the period after completion

Quarterly reconciliation is not sufficient for active businesses.

What Professional Reconciliation Looks Like

At Park East Bookkeeping, reconciliation isn’t just “making it match.”

It includes:

Matching to official bank statements

Reviewing unusual transactions

Confirming cleared items

Investigating discrepancies

Documenting adjustments

Locking prior periods

That’s financial oversight — not basic data entry.

Signs Your Business Needs Reconciliation Review

Ask yourself:

Has your bank account ever been “forced” to reconcile?

Are prior months documented?

Are books locked after closing?

Have reconciliations been skipped?

If you’re unsure, that’s usually the answer.

The Bottom Line

Bank reconciliation is not optional.

It is the control mechanism that keeps your financial reporting reliable, stable, and CPA-ready.

Without it, you’re making business decisions on numbers that may not reflect reality.

With it, you gain clarity, protection, and confidence.

If you’re a small business owner in the Greater Cleveland area and want structured monthly oversight — not guesswork — reconciliation is where it starts.

Call 440-533-9224 to learn more.